European Business Schools Librarian's Group

Finance Research Group Working Papers,

University of Aarhus, Aarhus School of Business, Department of Business Studies

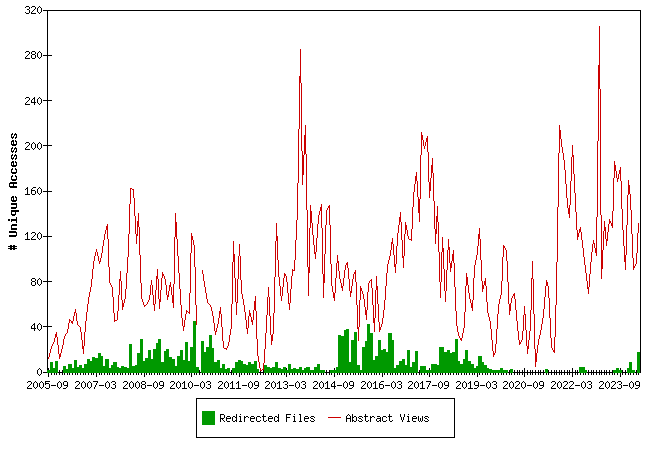

Downloads from EBLSG

Fulltext files are files downloaded from the EBLSG server, Redirected files are files downloaded from a server maintained by the publisher of a working paper series.

The statistics for 2010-06, 2012-04 (half month), 2012-05 and 2012-06 have unfortunately been lost. We regret this.

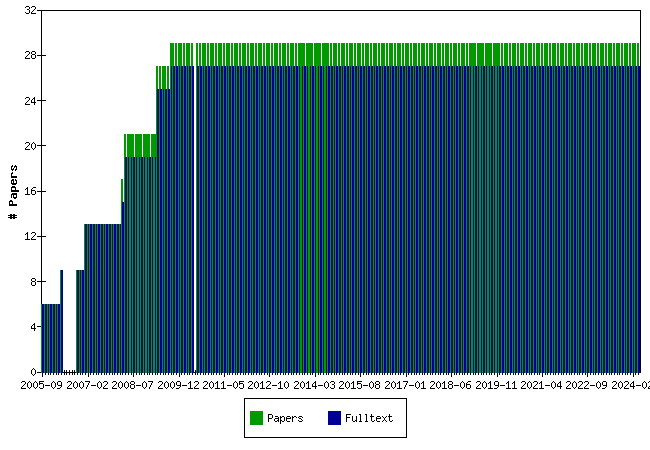

Papers at EBLSG

Top papers by Abstract Accesses last month (2026-06)

Top papers by Downloads last month (2026-06)

| Paper | Downloads |

|---|---|

| Pricing the Option to Surrender in Incomplete Markets Andrea Consiglio, Domenico De Giovanni | 6 |

| Sato Processes in Default Modeling Thomas Kokholm, Elisa Nicolato | 4 |

| Volatility and realized quadratic variation of differenced returns : A wavelet method approach Esben Høg | 3 |

| GSE Funding Advantages and Mortgagor Benefits: Answers from Asset Pricing Søren Willemann | 3 |

| The Fractional Ornstein-Uhlenbeck Process: Term Structure Theory and Application Espen P. Høg, Per H. Frederiksen | 3 |

| Pricing of Traffic Light Options and other Correlation Derivatives Thomas Kokholm | 3 |

| Investment decisions with benefits of control Thomas Poulsen | 2 |

| Debt and Taxes: Evidence from bank-financed unlisted firms Jan Bartholdy, Cesário Mateus | 2 |

| Traffic Light Options Peter Løchte | 2 |

| Do More Economists Hold Stocks? Charlotte Christiansen, Juanna Schröter Joensen, Jesper Rangvid | 2 |

| Investment Timing, Liquidity, and Agency Costs of Debt Stefan Hirth, Marliese Uhrig-Homburg | 2 |

Top papers by Abstract Accesses last 3 months (2026-04 to 2026-06)

| Paper | Accesses |

|---|---|

| Conducting event studies on a small stock exchange Jan Bartholdy, Dennis Olson, Paula Peare | 182 |

| The Fractional Ornstein-Uhlenbeck Process: Term Structure Theory and Application Espen P. Høg, Per H. Frederiksen | 141 |

| A Consistent Pricing Model for Index Options and Volatility Derivatives Rama Cont, Thomas Kokholm | 112 |

| Estimating US Monetary Policy Shocks Using a Factor-Augmented Vector Autoregression: An EM Algorithm Approach Lasse Bork | 106 |

| Traffic Light Options Peter Løchte | 97 |

| Decomposing European bond and equity volatility Charlotte Christiansen | 91 |

| Investment Timing, Liquidity, and Agency Costs of Debt Stefan Hirth, Marliese Uhrig-Homburg | 87 |

| Paying for Market Quality Amber Anand, Carsten Tanggaard, Daniel G. Weaver | 86 |

| Lapse Rate Modeling: A Rational Expectation Approach Domenico De Giovanni | 86 |

| On the Generalized Brownian Motion and its Applications in Finance Esben Høg, Per Frederiksen, Daniel Schiemert | 83 |

Top papers by Downloads last 3 months (2026-04 to 2026-06)

| Paper | Downloads |

|---|---|

| Conducting event studies on a small stock exchange Jan Bartholdy, Dennis Olson, Paula Peare | 25 |

| Sato Processes in Default Modeling Thomas Kokholm, Elisa Nicolato | 24 |

| Debt and Taxes: Evidence from bank-financed unlisted firms Jan Bartholdy, Cesário Mateus | 24 |

| Paying for Market Quality Amber Anand, Carsten Tanggaard, Daniel G. Weaver | 20 |

| Pricing the Option to Surrender in Incomplete Markets Andrea Consiglio, Domenico De Giovanni | 18 |

| Decomposing European bond and equity volatility Charlotte Christiansen | 17 |

| Estimating US Monetary Policy Shocks Using a Factor-Augmented Vector Autoregression: An EM Algorithm Approach Lasse Bork | 17 |

| The Fractional Ornstein-Uhlenbeck Process: Term Structure Theory and Application Espen P. Høg, Per H. Frederiksen | 16 |

| On the Generalized Brownian Motion and its Applications in Finance Esben Høg, Per Frederiksen, Daniel Schiemert | 16 |

| Pricing of Traffic Light Options and other Correlation Derivatives Thomas Kokholm | 16 |

Top papers by Abstract Accesses all months (from 2005-09)

| Paper | Accesses |

|---|---|

| A Consistent Pricing Model for Index Options and Volatility Derivatives Rama Cont, Thomas Kokholm | 1471 |

| The Fractional Ornstein-Uhlenbeck Process: Term Structure Theory and Application Espen P. Høg, Per H. Frederiksen | 1443 |

| Debt and Taxes: Evidence from bank-financed unlisted firms Jan Bartholdy, Cesário Mateus | 1345 |

| Danish Mutual Fund Performance - Selectivity, Market Timing and Persistence. Michael Christensen | 1326 |

| Traffic Light Options Peter Løchte | 1325 |

| Conducting event studies on a small stock exchange Jan Bartholdy, Dennis Olson, Paula Peare | 1304 |

| Realized Bond-Stock Correlation: Macroeconomic Announcement Effects Charlotte Christiansen, Angelo Ranaldo | 1302 |

| On the Generalized Brownian Motion and its Applications in Finance Esben Høg, Per Frederiksen, Daniel Schiemert | 1155 |

| Decomposing European bond and equity volatility Charlotte Christiansen | 1150 |

| Paying for Market Quality Amber Anand, Carsten Tanggaard, Daniel G. Weaver | 1138 |

Top papers by Downloads all months (from 2005-09)

| Paper | Downloads |

|---|---|

| Pricing the Option to Surrender in Incomplete Markets Andrea Consiglio, Domenico De Giovanni | 321 |

| The Fractional Ornstein-Uhlenbeck Process: Term Structure Theory and Application Espen P. Høg, Per H. Frederiksen | 164 |

| Danish Mutual Fund Performance - Selectivity, Market Timing and Persistence. Michael Christensen | 163 |

| Lapse Rate Modeling: A Rational Expectation Approach Domenico De Giovanni | 162 |

| Conducting event studies on a small stock exchange Jan Bartholdy, Dennis Olson, Paula Peare | 140 |

| Debt and Taxes: Evidence from bank-financed unlisted firms Jan Bartholdy, Cesário Mateus | 139 |

| A Consistent Pricing Model for Index Options and Volatility Derivatives Rama Cont, Thomas Kokholm | 113 |

| Decomposing European bond and equity volatility Charlotte Christiansen | 104 |

| On the Generalized Brownian Motion and its Applications in Finance Esben Høg, Per Frederiksen, Daniel Schiemert | 102 |

| Investment Timing, Liquidity, and Agency Costs of Debt Stefan Hirth, Marliese Uhrig-Homburg | 99 |

- University of Aarhus, Aarhus School of Business, Department of Business Studies

- Home page for this series

Questions (including download problems) about the papers in this series should be directed to Helle Vinbaek Stenholt ()

Report other problems with accessing this service to Sune Karlsson ().

This page generated on 2026-07-01 06:01:07.