European Business Schools Librarian's Group

Working Papers,

Copenhagen Business School, Department of Finance

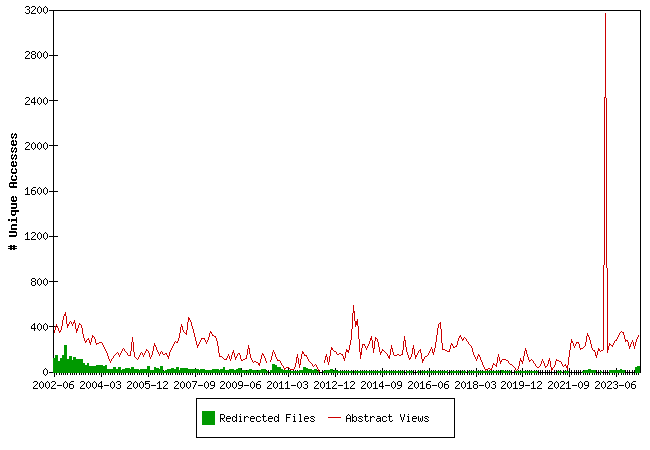

Downloads from EBLSG

Fulltext files are files downloaded from the EBLSG server, Redirected files are files downloaded from a server maintained by the publisher of a working paper series.

The statistics for 2010-06, 2012-04 (half month), 2012-05 and 2012-06 have unfortunately been lost. We regret this.

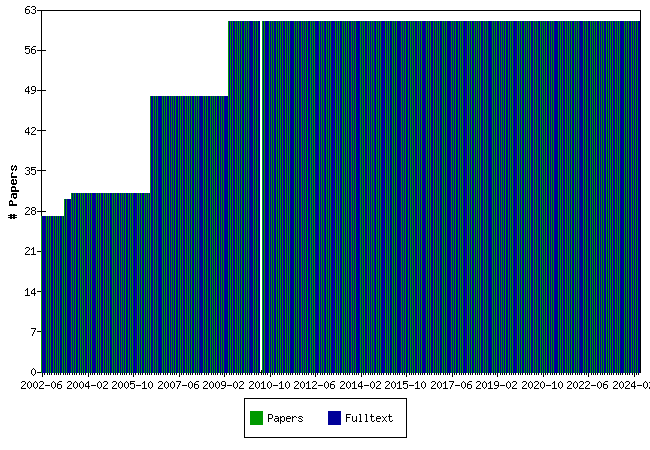

Papers at EBLSG

Top papers by Abstract Accesses last month (2026-06)

| Paper | Accesses |

|---|---|

| Seasonality in Agricultural Commodity Futures Carsten Sørensen | 43 |

| CEO Turnovers and Corporate Governance: Evidence from the Copenhagen Stock Exchange Robert Neumann, Torben Voetmann | 37 |

| Stochastic Volatility and Seasonality in Commodity Futures and Options: The Case of Soybeans Martin Richter, Carsten Sørensen | 37 |

| Empirical Rationality in the Stock Market Peter Raahauge | 37 |

| On Makeham's formula and xed income mathematics Bjarne Astrup Jensen | 36 |

| Foundation ownership and financial performance. Do companies need owners? Steen Thomsen, Caspar Rose | 34 |

| Optimal Consumption and Investment Strategies with Stochastic Interest Rates Carsten Sørensen, Claus Munk | 31 |

| Evidence on the Limits of Arbitrage: Short Sales, Price Pressure, and the Stock Price Response to Convertible Bond Calls Ken L. Bechmann | 30 |

| On Specific Performance in Civil Law and Enforcement Costs Henrik Lando, Caspar Rose | 30 |

| Accounting Transparency and the Term Structure of Credit Default Swap Spreads Claus Bajlum, Peter Tind Larsen | 29 |

Top papers by Downloads last month (2026-06)

Top papers by Abstract Accesses last 3 months (2026-04 to 2026-06)

Top papers by Downloads last 3 months (2026-04 to 2026-06)

Top papers by Abstract Accesses all months (from 2002-06)

Top papers by Downloads all months (from 2002-06)

Questions (including download problems) about the papers in this series should be directed to Lars Nondal ()

Report other problems with accessing this service to Sune Karlsson ().

This page generated on 2026-07-01 06:01:11.