European Business Schools Librarian's Group

Finance Working Papers,

University of Aarhus, Aarhus School of Business, Department of Business Studies

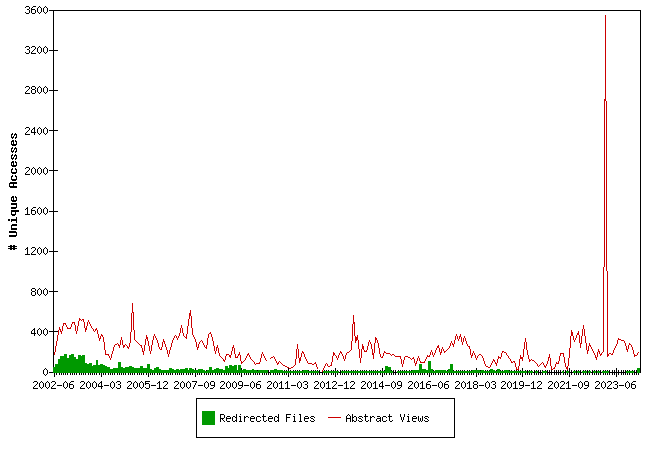

Downloads from EBLSG

Fulltext files are files downloaded from the EBLSG server, Redirected files are files downloaded from a server maintained by the publisher of a working paper series.

The statistics for 2010-06, 2012-04 (half month), 2012-05 and 2012-06 have unfortunately been lost. We regret this.

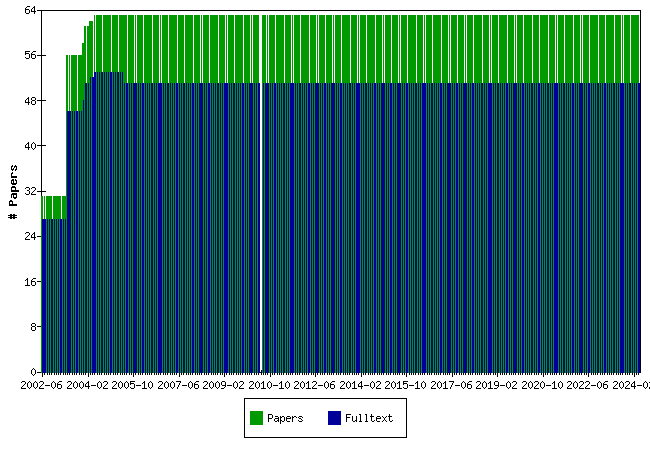

Papers at EBLSG

Top papers by Abstract Accesses last month (2026-06)

Top papers by Downloads last month (2026-06)

| Paper | Downloads |

|---|---|

| Finite Difference Computation of State-Prices in Term Structure Models: with Applications to Calibration and MBS Analysis Nicki Søndergaard Rasmussen | 7 |

| The comovement of US and UK stock markets. Tom Engsted, Carsten Tanggaard | 6 |

| Cross-Currency LIBOR Market Models. Peter Mikkelsen | 6 |

| Super-Efficient Prediction Based on High-Quality Marker Information Jens Perch Nielsen | 5 |

| Boundary and Bias Correction in Kernel Hazard Estimation Jens Perch Nielsen, Carsten Tanggaard | 5 |

| Errors in Trade Classification: Consequences and Remedies. Carsten Tanggaard | 4 |

| A New Daily Dividend-adjusted Index for the Danish Stock Market, 1985-2002: Construction, Statistical Properties, and Return Predictability Klaus Belter, Tom Engsted, Carsten Tanggaard | 4 |

| Misspecification versus bubbles in hyperinflation data: Comment. Tom Engsted | 4 |

| Quantifying the "Peso Problem" Bias: A Switching Regime Approach. Allan Bødskov Andersen | 4 |

| Volatility-Spillover E ffects in European Bond Markets Charlotte Christiansen | 4 |

Top papers by Abstract Accesses last 3 months (2026-04 to 2026-06)

| Paper | Accesses |

|---|---|

| Estimating the Consumption-Capital Asset Pricing Model without Consumption Data: Evidence from Denmark Anne-Sofie Reng Rasmussen | 132 |

| Variable Bandwidth Kernel Hazard Estimators Jens Perch Nielsen | 122 |

| Boundary and Bias Correction in Kernel Hazard Estimation Jens Perch Nielsen, Carsten Tanggaard | 119 |

| The Relation Between Asset Returns and Inflation at Short and Long Horizons. Tom Engsted, Carsten Tanggaard | 111 |

| The comovement of US and UK stock markets. Tom Engsted, Carsten Tanggaard | 104 |

| On the Suboptimality of Single-Factor Exercise Strategies for Bermudan Swaptions Mikkel Svenstrup | 99 |

| The Pros and Cons of Butterfly Barbells Michael Christensen | 99 |

| A New Test for Speculative Bubbles Based on Return Variance Decompositions. Tom Engsted, Carsten Tanggaard | 98 |

| Bootstrap Inference in Semiparametric Generalized Additive Models. Wolfgang Härdle, Sylvie Huet, Enno Mammen, Stefan Sperlich | 95 |

| Testing for Multiple Types of Marginal Investor in Ex-day Pricing Jan Bartholdy, Kate Briown | 95 |

Top papers by Downloads last 3 months (2026-04 to 2026-06)

Top papers by Abstract Accesses all months (from 2002-06)

Top papers by Downloads all months (from 2002-06)

- University of Aarhus, Aarhus School of Business, Department of Business Studies

- Home page for this series

Questions (including download problems) about the papers in this series should be directed to Helle Vinbaek Stenholt ()

Report other problems with accessing this service to Sune Karlsson ().

This page generated on 2026-07-01 06:01:08.